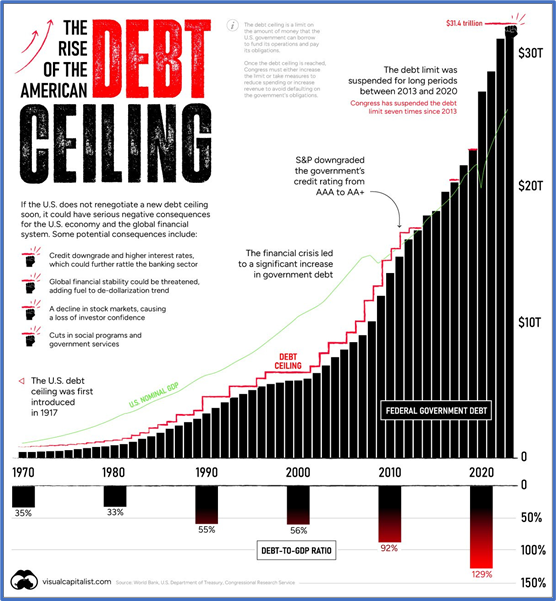

Debt Ceiling Kabuki Theater Continues with Congressional House and Presidential Administration Negotiators Reportedly Close to a Deal, but it’s not Finalized… Media outlets claim the two sides are within $70 billion in discretionary spending of reaching an agreement.

What it means— So, they pass a budget without planning to pay for it, set arbitrary limits on how much the government can spend, and then call it a crisis when the budget and spending cap collide. There’s enough blame to go around in this idiotic game of financial suicide, as we wait for members of both parties to put down their guns.

Instead of going through this charade every few years, dragging the nation and the investing world through it, why doesn’t Congress pass a law that the budget and debt limit for the next year must be passed at the same time? I’m guessing no one in Congress wants to give up their chance to grandstand, er, make a stand, on the issue. Here’s a forecast: we won’t default (in the meaningful way of not paying bills), and the nation won’t crumble. But we will have lots of drama and market volatility.

May Federal Reserve Meeting Minutes Show Lack of Consensus on Next Move… The voting members of the Federal Open Market Committee (FOMC) went back and forth about either raising rates again at the next meeting or stepping aside to see how higher rates affect the economy.

What it means— Amazingly, the minutes reflect exactly what Chair Powell said in the press conference after the meeting at the first of the month. The bankers don’t agree on the next move, the economic reports since then haven’t been clear, and the debt ceiling argument continues. The only thing that seems clear is that the central bankers don’t expect to cut rates this year, even though futures give that a 60% chance. The staff members at the Fed now expect a mild recession by year’s end. If that happens, we might get a 0.25% cut in December, but inflation would have to be close to 2% or even lower. Don’t hold your breath.

Personal Consumption Expenditures Index Rose 0.4% in April, Is Up 4.4% Over Last Year… The annual gain in the Personal Consumption Expenditures (PCE) Index increased from 4.2% in March.

What it means— Core PCE, excluding food and energy, also rose 0.4% last month and bumped up from 4.6% to 4.7% for the year. That’s not the right direction. Rising PCE on both the headline and core readings will give the central bankers more to consider when they next discuss raising rates.

Between now and the next Fed monetary policy meeting, investors will pay attention to the speeches by voting members looking for clues on the central bank’s next move, if any. While the bankers want to ensure orderly financial markets, their top priority at the moment is fighting inflation.

April New Home Sales Up 4.1% for Month and 12% Over Last Year… The median new-home sale price fell to $420,800, down from the peak of $496,800 last October.

What it means— Rising new home sales confounded analysts, as they expected that mortgage rates near 7% would hold down sales. But the name of the game is inventory—as in, there isn’t any. With existing home inventory below three months’ supply, buyers are piling into the new home market. It doesn’t hurt that builders cut prices this spring, although the share of builders dropping prices fell from 30% to 27% last month. The supply of new homes for sale fell 3.8% from March to April. At the current sale rate, the market has a 7.6-month supply.

While short supply usually drives prices higher, climbing mortgage rates are holding prices back. If the expected 500,000 apartments reach the market this year, then rents might ease a bit and take some pressure off of the real estate market. The reprieve won’t likely last long because so many Millennials want to buy homes, but any break in price would be welcome.

Initial Jobless Claims Fall After Massachusetts Fraud Detected… Once the fraud was scrubbed, the previous week’s total fell to 225,000 and this week’s claims inched up slightly to 229,000.

What it means— Another day, another supposedly weak economic indicator shows a sign of strength. In addition to jobless claims easing, continued claims inched down just a bit, from 1.799 million to 1.79 million. As pointed out often, these changes aren’t much in an economy with more than 160 million workers, but we’re looking for trends. So far, we’re not seeing signs that employment is softer, which will give the Fed cover if the bankers decide to boost rates by another 0.25% next month.

Woman Goes to Police Station in Stolen Car to Pick Up Teens Arrested for Stealing Cars… The Charles County, Maryland, Police Department stopped two stolen Hyundai vehicles on Crain Highway, but both sped away before the drivers could be questioned. The police found the occupants, four teens and two adults, in a nearby park-and-ride lot. The adults were charged and held, while the teens were charged as juveniles and set to be released. That changed after their guardian showed up at the police station in a stolen vehicle. The police said that all the suspects know each other. Perhaps they met in vocational school, where obviously they learned a trade.

Data supplied by HS Dent Research

“When the facts change, I change my mind.

What do you do?” ~ John Maynard Keynes

Our plan is “the plan will change.”

What is your plan?

Relative strength measures the price performance of a stock against a market average, a selected universe of stocks or a single alternative holding. Relative strength improves if it rises faster in an uptrend, or falls less in a downtrend. It is easily applied to individual positions in your portfolio and to sectors and asset classes.

A copy of our form ADV Part 2 is available online.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Investor Resources, Inc. (“Investor Resources”), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Investor Resources. Please remember to contact Investor Resources, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Investor Resources shall continue to rely on the accuracy of information that you have provided. Investor Resources is neither a law firm, nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Investor Resources’ current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at https://www.investorresourcesinc.com/. Clients Please Note: Advise us if you have not been receiving account statements (at least quarterly) from Charles Schwab & Co.™