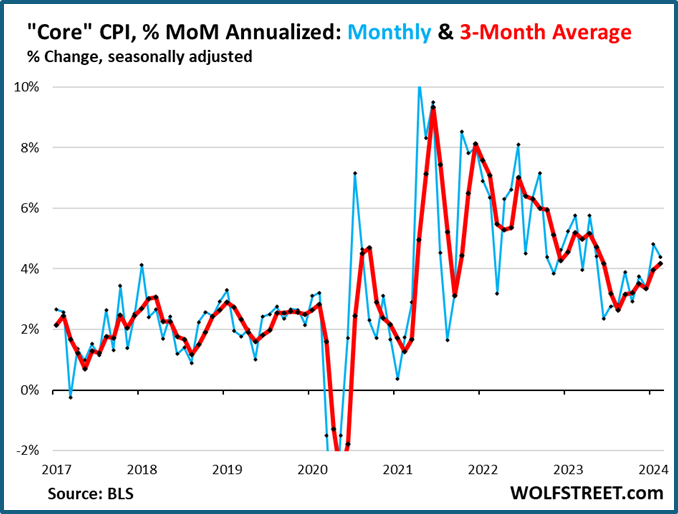

Consumer Price Index Rose 0.4% in February, Was Up 3.2% Over the Last Year… The core Consumer Price Index (CPI), excluding food and energy, fell to 3.8%, but it was higher than the forecast of 3.7%.

What it means— Inflation appears to have plateaued, or at least to have reduced the rate of deceleration to a crawl. That’s not good. Without solid deceleration, there’s no reason for the Fed to cut rates more than 0.25% when they cut. This could leave rates around 4.75% at the end of the year, with long bonds creeping higher. With geopolitical turmoil and a nasty election brewing, don’t expect the economy to sail smoothly for the rest of the year. But stranger things have happened. With inflation appearing in finished goods again ending the “deflationary” trend, big bets in bonds could fall apart.

Retail Sales Soft in February, up 0.4% Overall but Down 0.1% Once Autos are Excluded… The reports would have been worse if they had been adjusted for inflation.

What it means— Consumers are still going out to eat and hanging out in bars, but they are spending less in department stores and furniture stores. Core CPI has been rising since last June despite Mr. Market expecting the opposite.

Interestingly, people are spending more on building and gardening equipment. Maybe that’s because bushes that look like Charlie Brown’s Christmas tree are priced like the tree in Rockefeller Plaza. The price of annuals make you want to try your hand at a greenhouse next winter. Still, overall retail sales are sluggish, which could weigh on prices and inflation in the months ahead.

Producer Price Index Jumps 0.6% in January, Twice the 0.3% Expected… This is the second hot report in a row.

What it means— If producers are paying for it, eventually consumers will pay for it. The good news is that 70% of the jump is energy. While that doesn’t make it cost less for consumers, at least we know why—or at least we can tell ourselves this when we get to the checkout line.

Trump and Biden Gather Enough Votes in Primaries To Win Nominations… Biden essentially had no opponents, and Nikki Haley picked up very few delegates in her race with Trump.

What it means— Instead of a race between dumb and dumber, it’s old and older. It should boil down to a tale of two economies. Either way, the man that wins will be the oldest president in history. The next oldest is Biden, who edged out Trump in his first term. Why doesn’t this make us feel comfortable?

Data supplied by HS Dent Research

“When the facts change, I change my mind.

What do you do?” ~ John Maynard Keynes

Our plan is “the plan will change.”

What is your plan?

Relative strength measures the price performance of a stock against a market average, a selected universe of stocks or a single alternative holding. Relative strength improves if it rises faster in an uptrend, or falls less in a downtrend. It is easily applied to individual positions in your portfolio and to sectors and asset classes.

A copy of our form ADV Part 2 is available online.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Investor Resources, Inc. (“Investor Resources”), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Investor Resources. Please remember to contact Investor Resources, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Investor Resources shall continue to rely on the accuracy of information that you have provided. Investor Resources is neither a law firm, nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Investor Resources’ current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at https://www.investorresourcesinc.com/. Clients Please Note: Advise us if you have not been receiving account statements (at least quarterly) from Charles Schwab & Co.™