Existing Home Sales Fell 5.4% in June, Are Down 14.2% Over Last Year… Sales dipped to an annualized rate of 5.12 million, the lowest since June 2020. Excluding the pandemic, it was the lowest sales rate since January 2019.

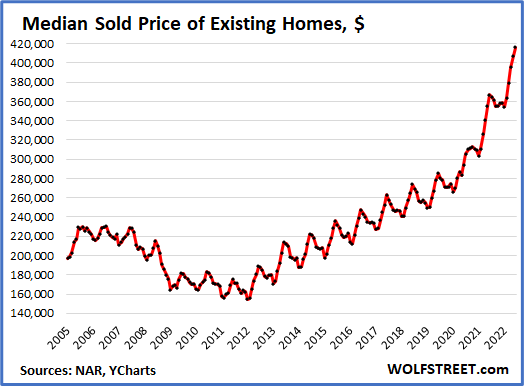

What it means— It is not surprising that substantially higher interest rates are eating into demand. It is surprising that, so far, prices continue to climb. The median existing home sale price set a record last month of $416,000, up 14.2% over last year.

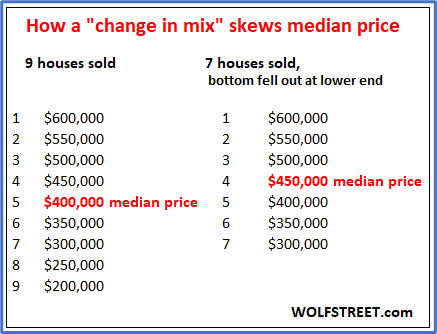

Sales haven’t changed all that much since higher priced homes are still selling as lesser priced homes falter. The median moves higher while prices can remain stable.

As we’ve discussed for years, it’s all about supply. The existing-home inventory rose 9.6% last month, to 1.26 million units. That’s the first year-over-year gain in three years, but it still brings inventory up to just three months of supply at the current sales pace. Homes were on the market an average of just 14 days last month, a new record low, although numbers go back only to 2011. Interestingly, first-time home buyers made up 30% of sales last month, up from 27% in May but still well below the long-term average of about 35%. Owners of two homes waiting for higher prices to sell the previously occupied house are beginning to list their vacant properties as sales slow and prices soften. This will add to inventory.

While inventory is the key to the housing market on the supply side, rising rents are keeping pressure on the demand side. First-time buyers might be wary of high prices and rising mortgage rates, but they’re not getting any relief by remaining in rentals, where landlords are raising rents. The Millennials are getting squeezed.

Housing Starts Fell 2% in June, Are Down 6.3% Over Last Year…Single-family construction fell 8%, but multi-family construction increased 15%.

What it means— Home builders aren’t blind or stupid. They’re cutting back to match the uncertainty in the economy as we march toward a recession and the Fed raises rates. Builders are reporting falling traffic in new homes for sale, and more contracts are falling through, but builders still have a backlog of orders.

The bottleneck in the new-home market is the same one in the existing-home market: inventory. If builders dramatically reduce the number of units they build, then we won’t create enough housing to meet current demand, which will keep prices from cratering.

Initial Jobless Claims Rise Above 250,000… Initial jobless claims rose from 244,000 to 251,000, a key psychological level.

What it means— Initial jobless claims edged higher, breaching the 250,000 mark for the first time since dropping below that level last November. With companies from Ford (NYSE: F) to Tesla (Nasdaq: TSLA) announcing layoffs and with others, such as Apple (Nasdaq: AAPL) and Alphabet (Nasdaq: GOOGL), either slowing in hiring or initiating a hiring freeze, we can expect more initial claims in the weeks ahead.

With the unemployment rate around 3.6%, this isn’t a problem, as long as you’re not among those who lose their jobs. Initial jobless claims are a coincidental indicator, whereas the unemployment rate is a lagging indicator. We’ll have to see if jobless claims walk higher at a moderate pace, which the economy could tolerate, or if claims suddenly spike, which would be a bad sign.

European Central Bank (ECB) Raises Rates for the First Time in Eleven Years… to Zero… The ECB raised the large depositor rate from negative 50 basis points to zero and gave a few more details about the Transmission Protection Instrument (TPI). The ECB also quit giving any forward guidance opting to “wait for data.”

What it means— With inflation running above 9% because of soaring energy and food prices, raising the overnight rate to zero isn’t going to do anything. The more important part of the announcement was about the bank’s new TPI, which allows the ECB to use funds from maturing bonds to buy other bonds from specific countries, such as Italy, to even out rising interest rates across the continent.

This is a thinly veiled rescue plan for Italy, Greece, and other nations that have watched their borrowing costs soar because investors think they might go under. Italy’s government has collapsed in part due to inflation. As the third largest regional economy with a debt ratio of 150%. As the ECB hikes rates, the risk of an Italian bond default increase. Shades of Greek bonds!

The ECB will use funds that belong to the entire economic bloc to prop up the bad actors, which is exactly what German banking officials said the ECB would do when they hesitated to join the monetary bloc more than 20 years ago. The more firepower the ECB uses to support the weak economies, the lower the euro will fall.

Irishman Buys a Plane Ticket Just to Search for his Luggage… Dermot Lennon flew home from Australia to Dublin at the end of June, but the airline told him that his luggage didn’t make the trip. After waiting for hours, he went home, but he then found himself and his luggage in a sort of travel purgatory, just like many other passengers this summer. Lennon’s bag joined the thousands of other bags that currently are lost. Due to severe staffing shortages, airlines aren’t making much headway in reuniting people with their luggage.

Lennon decided to take matters into his own hands. He returned to the airport a week later to search for his bag but wasn’t allowed into the baggage area, because he wasn’t a ticketed passenger. Lennon then purchased the cheapest ticket he could find (an $18 flight to Glasgow), passed through security, and went straight for the baggage area. After searching for hours, he found his luggage among thousands of other bags, many of which appeared to have been there for weeks. Perhaps the airlines could start a new service. For a fee, they could actually search for your bag that they lost.

Data supplied by HS Dent Research

“When the facts change, I change my mind.

What do you do?” ~ John Maynard Keynes

Our plan is “the plan will change.”

What is your plan?

Relative strength measures the price performance of a stock against a market average, a selected universe of stocks or a single alternative holding. Relative strength improves if it rises faster in an uptrend, or falls less in a downtrend. It is easily applied to individual positions in your portfolio and to sectors and asset classes.

A copy of our form ADV Part 2 is available online.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Investor Resources, Inc. (“Investor Resources”), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Investor Resources. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Investor Resources is neither a law firm, nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Investor Resources’ current written disclosure Brochure discussing our advisory services and fees is available upon request or at https://www.investorresourcesinc.com/. Please Note: If you are a Investor Resources client, please remember to contact Investor Resources, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Investor Resources shall continue to rely on the accuracy of information that you have provided. Please Note: If you are an Investor Resources client, Please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.