Federal Reserve Chair Jerome Powell Gives Interview on Television Show 60 Minutes… Powell discussed where we are in the monetary cycle and the forecasts of the voting members of the Federal Open Market Committee (FOMC).

What it means— In some ways, this seemed like Powell was an irate parent lecturing his children as he wags his finger, while the children stick their fingers in their ears and blow big raspberries. How else do you explain the chair of the Federal Reserve, who holds a one-hour, solo press conference after several monetary policy meetings a year, booking an appearance in prime time to tell us the same thing? Economy doing alright? Got it. Hold rates higher a little longer to make sure inflation is in check? Yep.

Going to watch the economic reports for (data-driven) surprises? Yessir. It’s doubtful the interview changed any minds. The people who forecast five or six rate cuts this year instead of the two or three estimated by the voting members of the FOMC still think they are right, no matter what Powell says.

Border Control and Immigration Deal Dies… A Senate proposal that tied support for Ukraine and Israel to tighter border controls is DOA.

What it means— The dead legislation is a reminder that politics are alive and well in Washington, where striving for office is more important than the American population. Over three million illegal immigrants streamed across our southern border last year (a record), which sounds like something we should address. Republicans have whipped the Biden administration with the crisis for years. Unwilling and then unable to stop it, and seeing the issue as Kryptonite in the coming election, Biden & Company relented in many areas, earning the ire of the left. But he didn’t have anything to fear.

Republicans, seeing the border issue sliding off the list of issues in the election, refused to play ball. The current proposal includes gaps and loopholes you could drive a truck through. To say it wasn’t perfect is an understatement. But it’s the closest that the two parties have been to a deal in more than two decades and is light-years from Biden’s position at the start of his term. When everyone is mad, you know you’re in the right area to compromise. For our sake, let’s hope they use the next week or so to revise the legislation and pass it, but it doesn’t look likely.

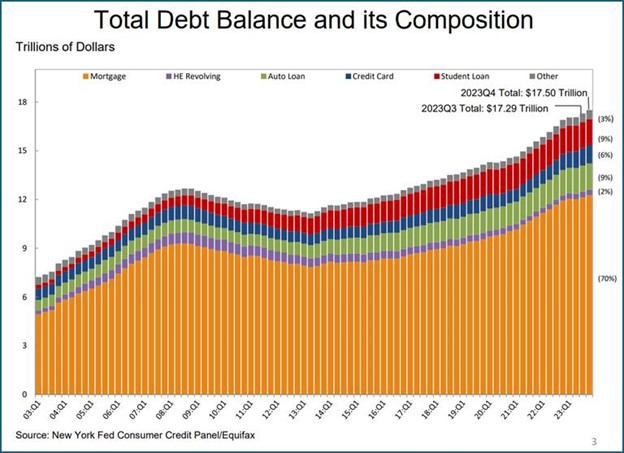

Consumer Debt Reached a Record $17.5 Trillion in Fourth-Quarter 2023… Among the numbers, mortgage debt rose $112 billion, while revolving debt increased $50 billion.

What it means— Aggregate household debt balances increased by $212 billion (+1.2%) in the 4th quarter of 2023 to reach a total of $17.5 trillion. The household debt load has increased $3.4 trillion since the onset of the pandemic, despite record government stimulus and a lengthy moratorium on various debt obligations and household expenses. Mortgage balances were largely unchanged and stood at $12.25 trillion at the end of December.

This is where math and context take the power out of the headline. For math, we should ask about nominal versus inflation-adjusted numbers. It’s not a record once it is adjusted, and after searing inflation over the last three years, such adjustments will be important. When inflation bumped along at 1.5% or so during the 2010s, adjusting for inflation wasn’t such a big deal. Now, after clocking almost 9% in one year and near 4% in two others, it will make a much bigger difference.

As for context, how much does consumer credit take out of your annual budget? The Federal Reserve of St. Louis shows that household debt servicing eats up 9.77% of our disposable income, a little less than in 2019. What they didn’t mention is that, except for the pandemic, this is the lowest percentage of personal income needed to service household debt since records began in 1980. You’d think they would mention that.

The problem is that income and debts aren’t equally distributed. If younger workers are taking on more debt to live and now are working fewer hours, we could see this cohort get squeezed this year. So far, they’re still willing to burn up the credit cards.

You Know You’re a Redneck, or Perhaps a Brit, When Many of Your Friends Are Missing Teeth… In Britain, it’s tough to get a dental appointment. A recent survey found that 25% of consumers couldn’t get an appointment, with a full 90% of new patients turned away. The problem is not a lack of dentists, it’s that the National Health System (NHS) pays little for service. If Brits are willing to pay for private dental care, they have plenty of options, but that rankles Brits who have paid into the NHS all of their lives just to find out they can’t use it. For those who can’t pay for private care, the options can be ugly. Some live with the pain of rotting teeth, while others resort to pulling them out themselves. As the saying goes, “If you think care is expensive now, just wait until the government makes it free.”

Data supplied by HS Dent Research

“When the facts change, I change my mind.

What do you do?” ~ John Maynard Keynes

Our plan is “the plan will change.”

What is your plan?

Relative strength measures the price performance of a stock against a market average, a selected universe of stocks or a single alternative holding. Relative strength improves if it rises faster in an uptrend, or falls less in a downtrend. It is easily applied to individual positions in your portfolio and to sectors and asset classes.

A copy of our form ADV Part 2 is available online.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Investor Resources, Inc. (“Investor Resources”), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Investor Resources. Please remember to contact Investor Resources, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Investor Resources shall continue to rely on the accuracy of information that you have provided. Investor Resources is neither a law firm, nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Investor Resources’ current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at https://www.investorresourcesinc.com/. Clients Please Note: Advise us if you have not been receiving account statements (at least quarterly) from Charles Schwab & Co.™