The Federal Reserve Held Monetary Policy Steady… The central bankers announced that they will hold rates at 0% to 0.25% and continue to purchase $120 billion in bonds each month.

What it means— No change. They could have saved us a bunch of time and anguish in their published statement and then in Chair Powell’s comments in the press conference by simply saying, “No change.”

But not changing their policy isn’t the same as doing nothing. The bankers are pumping massive amounts of money into the financial system, which is driving asset inflation by driving down interest rates. Anyone who studied economics in college will say that we can’t have economic growth above 6%, inflation above 5%, and long-term interest rates at 2%. By cramming down rates, the Fed is forcing investors into other assets and giving borrowers more money to use when buying homes and cars. It’s great if you already own assets, but not so much if you’re trying to snag that first home.

Mr. Powell slipped in his comments revealing a significant clarification. As used by the Fed “transitory” refers to inflation’s “rate of change” and not a reduction in future prices. It is time to rethink future purchases to buying now instead of higher prices later – something the Fed wants to avoid.

Second-Quarter GDP Grows 6.5%, Below Expectations of 8.5%… The headline number was barely ahead of the 6.4% annualized growth in the first quarter.

What it means— The economy slowed a bit in late May and June, but not enough to drag down GDP by 2%. A quick look at the components reveals the biggest issue: inventories fell again. Private businesses couldn’t keep up with sales and restock at the same time, so inventories fell and pulled down second-quarter GDP by 1.13%. With the holiday season around the corner, we can expect this number to turn up next quarter and give GDP a corresponding boost. As hard as it is to believe, the government spent a bit less in the second quarter, which also weighed on the numbers.

On the positive side, consumer spending jumped 7.78%. There are many questions about third and fourth quarter GDP. By year’s end, more people are expected to return to work (a positive) and the government stimulus spending wears off (a negative). Most people agree that by late 2022, we should be back to about the 2% growth of the 2010s.

New Home Sales Slump in June… New-home sales fell 6.6% last month as buyers complained about high prices and thin inventory.

What it means— After reaching the highest level in almost 15 years, new-home sales dropped back to the level of April 2020, when no one was sure how the pandemic would play out. While sales then were held down by uncertainty, today they’re held down by prices.

The median sales price dipped from the all-time high of $380,700 in May to $361,000 last month, but that’s still more than 12% higher than a year ago. Slower sales translate into higher inventory, which rose to 6.3 months’ worth of homes at the current sales rate. This might be an early sign of real estate prices stabilizing as buyers balk at ever-higher prices, but it’s unlikely to signal a downturn.

There are new institutional investors in single family housing. Strength in the Single Family Rental segment is not diminishing. As long-term investors needing income which is no longer available from bonds, pensions and insurance companies with staying power and need are buying single family homes to rent. Teacher Retirement System of Texas and Pacific Life Insurance Company are investing with Tricon Residential, Inc., (CNGF) an owner of one of the largest pools of residential rentals. What they get is a rising income stream and an appreciating asset which is no longer available in fixed income. D.R. Horton (DHI) recently sold a 124 home development to a single purchaser, Fundrise LLC, that manages rentals for thousands of investors. While institutions are buyers, they are still less than 50% of purchasers.

Durable Goods Orders Rose 0.8% in May, Short of the 2% Forecast… Orders for goods that last more than three years ticked higher but were held back by inventory shortages in items such as cars.

What it means— Orders for aircraft increased 17%, which helped drive the headline number higher, even as orders for new cars fell 0.3%. Orders for non-defense goods excluding aircraft, a proxy for business spending, increased 0.5%. Consumer spending is decelerating a bit, but businesses are still spending as they try to catch up after being surprised by increased spending during the pandemic. It will likely take businesses the at least the rest of the year to normalize their inventories and supply chains.

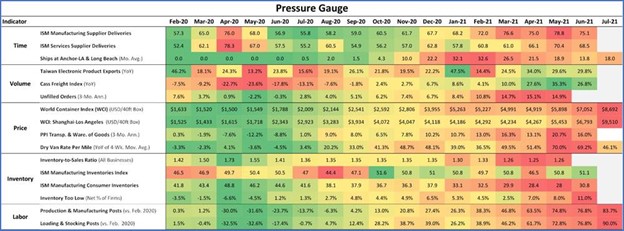

Wells Fargo published the graph below in a supply chain report revealing there is little relief in shipping problems. “It suggests that bottlenecks are not yet easing in any widespread fashion, let alone close to being fully resolved”. The conclusions reached by Wells Fargo align with the reasons for missed expectations seen in Thursday’s second quarter GDP report.

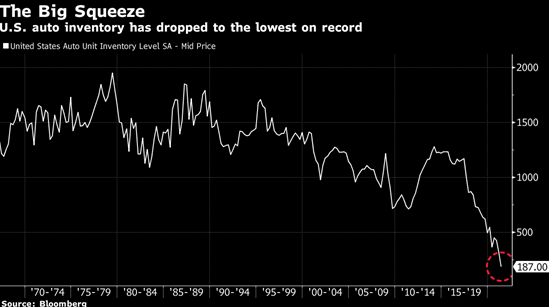

One of the bottlenecks is the lack of semiconductors which are used in most everything that uses electrical power. This is particularly evident on car lots with production largely limited to high profit models. U.S. auto inventories are at the lowest levels on record – since 1967. Whether it is empty lots or unheard-of mark-ups, the problem isn’t disappearing any time soon.

Six States Ban the Sale of Gaming Computers with Certain Graphics Chips Due to Excess Power Use…Under a 2017 law that just went into effect, California, Colorado, Hawaii, Oregon, Vermont, and Washington banned the sale of gaming PCs, Dell Alienware units, that contain the Nvidia GeForce RTX 3070 graphics card. The measure stemmed from a 2016 research report showing that gaming consumed 4.1 terawatts of electricity in California that year at a cost of $700 million. The report also noted that consoles such as PlayStations consumed two thirds of the power, yet only gaming PCs were banned.

Gamers don’t seem overly concerned. They often upgrade their computers anyway, and the offending graphics card can still be ordered separately by consumers in the states.

Data supplied by HS Dent Research

“When the facts change, I change my mind.

What do you do?” ~ John Maynard Keynes

Our plan is “the plan will change.”

What is your plan?

Relative strength measures the price performance of a stock against a market average, a selected universe of stocks or a single alternative holding. Relative strength improves if it rises faster in an uptrend, or falls less in a downtrend. It is easily applied to individual positions in your portfolio and to sectors and asset classes.

A copy of our form ADV Part 2 is available online.

Investor Resources, Inc. only transacts business in states where it is properly registered or notice filed, or excluded or exempted from registration requirements. Follow-up and individualized responses that involve either the effecting or attempting to effect transactions in securities, or the rendering of personalized investment advice for compensation, as the case may be, will not be made absent compliance with state investment adviser and investment adviser representative registration requirements, or an applicable exemption or exclusion.