Consumer Prices Rose 0.2% in July, Are Up 3.2% Over Last Year… Core inflation also rose 0.2% last month and is up 4.7% over last year.

What it means— Annual inflation rose a bit last month while core inflation eased, but both measures remain well above the Fed’s 2% target. The shelter component, up 0.4% for the month and 7.7% for the year, was the biggest contributor. We’re still waiting for shelter to catch down to real-time measures that showed lower home prices and flat rent last year, but time is running out.

Inflation is cooling but prices aren’t falling where it matters, at home where groceries are more expensive. However, on-line shopping is less expensive for eleven consecutive months.

Home prices and rents appear to have firmed in the last couple of months, although that might not last. Energy is another wild card for inflation. Oil prices jumped after mid-summer as the OPEC+ supply cuts worked through the market. OPEC+ and Russia production cuts will extend into September.

Despite China’s slowing economy, its need for oil remains robust. Along with global growth, the IEA forecasts more of the same with oil prices rising further with Brent briefly above $88 this week. If oil keeps moving closer to $100 per barrel, inflation will tick a bit higher and remain sticky. Record global demand in June was for 103 million bpd with August demand expected to be even higher. Gasoline futures aren’t confirming the end of inflation or the success of raiding the SPR.

July Producer Price Index Rose 0.3%…The Producer Price Index (PPI) measures the average selling price received by producers of goods and services.

What it means— What CPI giveth, PPI taketh away. Producer prices increased a bit more than people were expecting, which put the possibility of a September Fed rate hike back on the table one day after the tame Consumer Price Index (CPI) numbers appeared to make such a move unlikely. When Chair Fed Powell told us that the central bank was data dependent, he failed to describe the situation correctly. Because of the Fed’s stance, we’re all data dependent, left to parse every report and then buy or sell appropriately. It should be a volatile month in the markets.

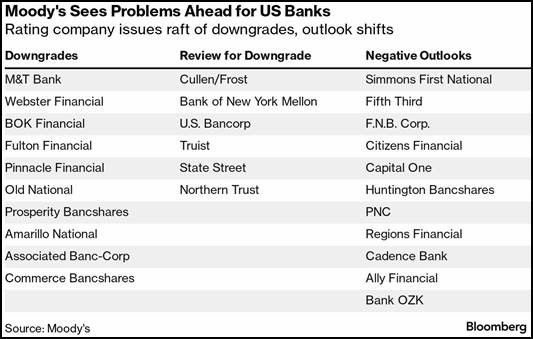

Moody’s Rating Services Downgrades Ten Regional Banks and Puts Sixteen on Notice… Citing deteriorating collateral for outstanding loans and other issues, Moody’s reduced the rating of several banks, which will make it more expensive for these lenders to borrow funds.

What it means— And so it begins. For the past two years, we’ve pointed out the problems created by the massive move to remote work, with declining commercial real estate values at the top of the list. As downtown leases come up for renewal, tenants are either closing offices or substantially reducing their square footage. Falling rents combined with rising refinancing rates and soaring hedge costs give commercial building owners plenty of reasons to mail the keys to their lenders.

When the mortgage rate jumped to 8.8% it’s time to jump ship, and that’s exactly what Ashford Hospitality Trust (AHT) did with jingle mailing the keys to 19 hotel properties. The mortgages are held in three separate CMBS portfolios that will bear the loss. Extending the loans required an unattractive down payment. The commercial real estate problem is industry wide and will have more entities following this path.

But the pain doesn’t stop at the bank or yield hungry investors. Ancillary businesses that supported office workers, from dry cleaners to restaurants, already have shut down, while city property tax collections will fall with declining valuations.

And Moody’s bank downgrades are expected to expand to larger firms.

We’ll need to wait to see what new trick the Fed will pull out of its hat to hold back this tidal wave.

Consumer Credit Nears $5 Trillion, Was Up $17.8 Billion in June… The growth in debt was in non-revolving credit, such as autos and student loans. Credit card debt eased slightly.

What it means— And this surprises no one. With interest rates more than double what they were at the beginning of 2022, loan payments are more expensive, which means borrowers take on more principal so that they can afford the payments. We can’t add debt forever, but consumers are in a strong financial position, with savings in the bank and job security. When the debt bomb blows up, it likely will be in commercial real estate, not personal finance.

Initial Jobless Claims Up 21,000 Last Week, to 248,000… Continued claims fell by 8,000, to 1.64 million.

What it means— It feels like a wash, rinse, repeat sort of report, but maybe not. Perhaps the still-strong employment picture is the story. In the face of prices rising on, well, everything, consumers are still out there buying stuff, which keeps companies on the hunt for workers. Adding in hundreds of billions of dollars of government spending financed by issuing debt doesn’t hurt today, but it might make tomorrow subdued as we deal with a looming debt hangover.

Texas Woman Battles Snake, Then Hawk, While Mowing her Lawn… Peggy Jones, 64, of Silsbee, TX, was mowing her lawn late on July 25 when a large snake fell from the sky and landed on her. The snake wrapped around her arm, and the more she tried to shake it off, the tighter it gripped her, biting at her face and spewing what she presumed to be venom at her. Then, a hawk descended on Jones, flapping its wings at her while pecking her and scratching her with its talons as it tried to get the snake.

Apparently, the hawk had caught the snake, dropped it onto Jones, and then set about getting its dinner back. Jones ran screaming toward her husband, and then the hawk flew off with the snake. Jones’ husband took her to the ER, where after hearing her story the doctor asked if she was on drugs. The physician determined she wasn’t bitten by the snake, bandaged her arm, and gave her antibiotics.

Data supplied by HS Dent Research

“When the facts change, I change my mind.

What do you do?” ~ John Maynard Keynes

Our plan is “the plan will change.”

What is your plan?

Relative strength measures the price performance of a stock against a market average, a selected universe of stocks or a single alternative holding. Relative strength improves if it rises faster in an uptrend, or falls less in a downtrend. It is easily applied to individual positions in your portfolio and to sectors and asset classes.

A copy of our form ADV Part 2 is available online.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Investor Resources, Inc. (“Investor Resources”), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Investor Resources. Please remember to contact Investor Resources, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Investor Resources shall continue to rely on the accuracy of information that you have provided. Investor Resources is neither a law firm, nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of Investor Resources’ current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at https://www.investorresourcesinc.com/. Clients Please Note: Advise us if you have not been receiving account statements (at least quarterly) from Charles Schwab & Co.™