Have you ever said, “the more things change, the more they remain the same?” That certainly is no longer true for our daily lives due to Covid-19’s impact on society here and abroad.

However, applied to the stock and bond market the adage remains applicable. Reflecting on the last bear market of 2008-09 we are compelled to look at the actions of the Federal Reserve. In that era, Wall Street banks bought mortgages, assemble an assortment of mortgages into investment offerings with attractive interest payouts. Theoretically, the diversification reduced risk. There is a lot of theory that does not work in real life. When the “junk credit status” of the investments became clear, liquidity disappeared, and prices collapsed. Wall Street Bankers were caught holding unmarketable securities.

The Fed implemented the Primary Dealer Credit Facility (PDCF) and provided bail out for the “too big to fail” banks. The PDCF is back in business making loans to banks and hedge funds. In the financial arena, this is referred to as “cash for trash.” This time it is not mortgages. It is bonds of barely credit worthy firms. The bonds have allowed some companies in the oil business to operate as oil prices fell. Other companies borrowed just to buy back their stock propping up the price and artificially enhance corporate earnings. As with all shenanigans, reality catches up.

If you have read our blogs, we have mentioned that something was wrong with bond market prices. It caused our portfolios to sell bonds and hold cash prior to the major stock market price collapse. That decision was good in that portfolios have been protected from major losses.

The Fed’s injection of liquidity has stabilized bond market pricing. However, the “cash for trash” program continues.

The Fed is now intervening directly in:

1) The Treasury markets (U.S. sovereign debt).

2) The municipal bond markets (debt issued by states and cities).

3) The corporate bond markets (debt issued by corporations).

4) The commercial paper markets (short-term corporate debt market).

5) The asset backed security market (everything from student loans to Certificates of

Deposit and more).

At this rate, we are watching for the Fed to become a direct buyer of stocks following Japan’s example. It is already a buyer of junk bonds though acquisition of ETFs. As this quarter unfolds, corporate earnings reports will reveal the initial economic damage from shutting down many businesses and non-commercial institutions. More time is needed to evaluate the broader effect on employment and financial health of businesses and households. With retail sales falling 8.7% from last March, unemployment above 20%, global oil supply substantially greater than demand, housing starts and industrial production at new lows, it will be July before data begins to reflect the magnitude of the economic down turn.

At the time of writing, there is no consensus on how or when to “restart” our economy. Regardless of the plan or timing, we will be faced with a decision of how much continuing risk of infections will we accept with or without social distancing. There is no easy answer for any of us as we adapt to the pandemic’s risks.

As for our lives, this time is different. It is the same for the markets. Never have economies shut down as in this year. How families and businesses survive, even with government efforts to supplement income or modify debt payments, remains unknown. Unemployment is expected to exceed 20 percent. Government programs are not large enough to bail out every business or household. What we do know is that we are all in this together.

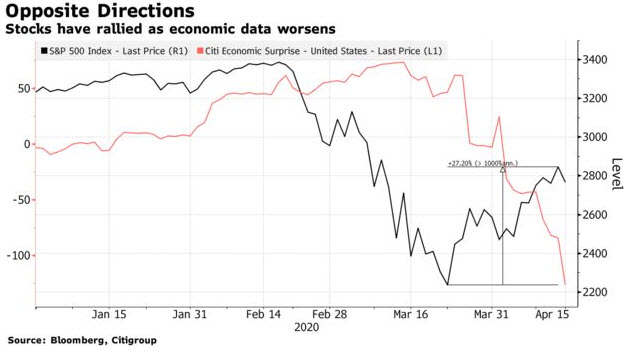

Within the markets, there are always buyers and sellers. The makeup of the parties varies with market conditions. After market declines, some normally reluctant investors view lower prices as bargains and become buyers. They are known as “buy-the-dip” investors. Many have been buying in the recent rally. On the surface, recent buyers of the dip have been ignoring changing economic conditions. Assumptions for the rally are based on quick return to full employment and short-term disruption from social distancing. Our view remains hopeful but requires more data confirmation before expanding our client’s risk exposure.

What we are looking for is buying by major investors known as the Dark Pools. They control the long-term investments of pension plans and mutual funds. They are very serious about not paying too much for any stock or bond. So far, in the current stock rally, the managers of the dark pools have remained on the sidelines. In the rally, they have continued reducing risk exposure by selling into rising prices.

The major Wall Street firms have a different duty. Their job is to be a buyer for any seller when there aren’t enough sellers to maintain liquidity. The Fed provides cash for the firms to do their job and avoid a more serious collapse if sellers had no buyer for their securities. This is a market condition that many investors have not experienced. It did occur in the ’08-’09 decline. It only lasted a few months. Hopefully, the efforts to stop the spread of Covid-19 will work quickly and a return to normal life and work soon follow. We continue our searching through market data watching for reasonable opportunities to add to our portfolios.

Question? Call us. 800-317-9119.